Wink Inc.

Enrolled Agents

America’s Tax Experts

®

Wink Tax Services

Tax Planning for Retirees: Social Security and Medicare Tax Rates.

Control Your Destiny

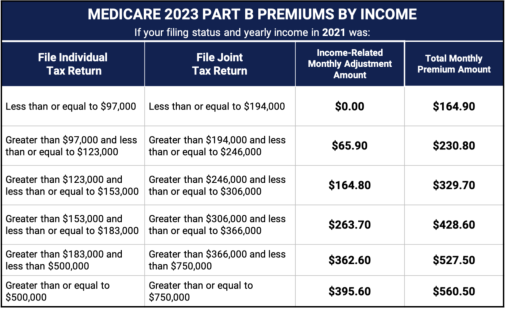

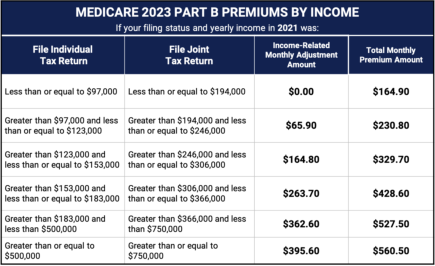

Medicare Tax Brackets Most begin Medicare at age 65, but did you know that your Medicare premium is based on your Modified Adjusted Gross Income from two years prior? That means that Medicare brackets matter as early as age 63. As we look at Medicare premium brackets and income each year, there's an additional complexity to be aware of. Medicare premium brackets are based on Modified Adjusted Gross Income (MAGI), which means they are unaffected by the standard or itemized deductions. As a result, income planning becomes more critical in Medicare brackets because you cannot offset your MAGI with mortgage interest, property tax, or charitable deductions.Income Planning for Medicare Premium Brackets

So, we know this is an important consideration, but let's quantify just how important by looking at the Medicare premium brackets. The lowest monthly premium for Medicare is $170.10 per month per person, but the highest Medicare bracket is $578.30 per month. So, that's a $9,796.80 annual cost variance between the bottom and top bracket for those married filing jointly. Unlike income tax brackets where only the marginal dollars are taxed at the next tax bracket, when considering Medicare brackets, even just one additional dollar of MAGI will push your premiums to the next bracket for an entire year. IRMAA [Income Related Monthly Adjustment Amount] 2023What Is IRMAA? [Income Related Monthly Adjustment Amount]

Medicare imposes surcharges on higher-income beneficiaries. The theory is that higher-income beneficiaries can afford to pay more for their healthcare. Instead of doing a 25:75 split with the government, they must pay a higher share of the program costs. The surcharge is called IRMAA, which stands for Income-Related Monthly Adjustment Amount. According to the Medicare Trustees Report, 8% of Medicare Part B and Part D beneficiaries paid IRMAA. The extra premiums they paid lowered the government’s share of the total Part B and Part D expenses by two percentage points. Big deal? The income used to determine IRMAA is your AGI plus muni bond interest from two years ago. Your current year income determines your IRMAA in 2 years. Your 2021 income determines your IRMAA in 2023. Your 2022 income determines your IRMAA in 2024. The untaxed Social Security benefits aren’t included in the income for determining IRMAA. As if it’s not complicated enough for not moving the needle much, IRMAA is divided into five income brackets. Depending on the income, higher-income beneficiaries pay 35%, 50%, 65%, 80%, or 85% of the program costs instead of 25%. The lines drawn for each bracket can cause a sudden jump in the premiums you pay. If your income crosses over to the next bracket by $1, all of a sudden your Medicare premiums can jump by over $1,000/year. If you are married and both of you are on Medicare, $1 more in income can make the Medicare premiums jump by over $1,000/year for each of you. IRMAA Appeal If your income two years ago was higher because you were working at that time and now your income is significantly lower because you retired (“work reduction” or “work stoppage”), you can appeal the IRMAA assessment. The “life-changing events” that make you eligible for an appeal include: • Death of spouse • Marriage • Divorce or annulment • Work reduction • Work stoppage • Loss of income from income producing property • Loss or reduction of certain kinds of pension income You file an appeal by filling out the form SSA-44 to show that although your income was higher two years ago, you had a reduction in income now due to one of the life-changing events above. For more information on the appeal, see Medicare Part B Premium Appeals.Not Penalized For Life

If your income two years ago was higher and you don’t have a life-changing event that makes you qualify for an appeal, you will pay the higher Medicare premiums for one year. IRMAA is re-evaluated every year as your income changes. If your higher income two years ago was due to a one-time event, such as realizing capital gains or taking a large withdrawal from your IRA, when your income comes down in the following year, your IRMAA will also come down automatically. It’s not the end of the world to pay IRMAA for one year. Roth Conversions Impact on Medicare Premiums Let's look at an example: Steve and Sara are both 63 years old, and they both have retired after successful careers. They do annual tax planning and make withdrawals from their after-tax accounts to fund living expenses so that they can do Roth conversions annually. Last year, at age 62, the only brackets they had to worry about were the income tax and capital gains tax brackets. However, at age 63, we need to start looking at their Medicare bracket. After retiring, Steve and Sara each receive pension benefits of $80,000 annually which puts them in the 22% income tax bracket for 2022. In addition, they take the standard deduction of $25,100. They also have substantial savings in IRAs and expect to have significant required minimum distributions at age 72 without taking any action. Previously, they converted IRA savings to Roth to max out their 22% income bracket, converting about $43,250 per year, which will reduce the size of their RMDs at age 72 and beyond). If they fail to think about Medicare brackets and Steve and Sara convert the same amount this year ($43,250), they will increase their Medicare premiums at age 65 from $170.10 per person per month to $238.10 per person per month. The annualized difference is approximately $1,600, but the effective tax rate on the conversion of $43,250 is now 25.7% instead of 22%. While this is only a $1,600 increase annually, it can add up year-over-year to a relatively significant number.The Common Mistake of DIY Tax Planning

Many choose to be even more aggressive to take advantage of the tax arbitrage provided by Roth conversions. For example, let's say that Steve and Sara know that their tax bracket will be significantly higher in the future than it is currently (22%). Therefore, they have been maxing out the 22% bracket and the 24% bracket, paying increased taxes now for lower required minimum distributions and associated taxes in the future. By doing this in 2022, they blow through the first few Medicare premium brackets and find themselves paying $442.30 each per month, an almost $5,000 annual increase in premiums per year. The effective tax rate on this conversion of $194,949 is 26.05% (24% ordinary income plus the additional Medicare premium of 2.05% ($5,000/$194,949). In this example, if Steve and Sara converted just $25,000 less, they could find themselves in a lower premium bracket with a lower effective tax rate of 25.6%. By properly planning their Roth conversions with a professional, they could save on premiums and taxes while also reaping the advantages of Roth conversions. These premiums may not be excessive enough to outweigh the benefits reaped from Roth conversions. Still, it is worth discussing converting slightly less in a given year to put them in a lower Medicare premium bracket. As noted, if you don't do this type of planning annually, the total premium increase year after year can add up! Remember, one dollar of MAGI can make the difference between a lower and higher Medicare bracket.Social Security Tax Brackets

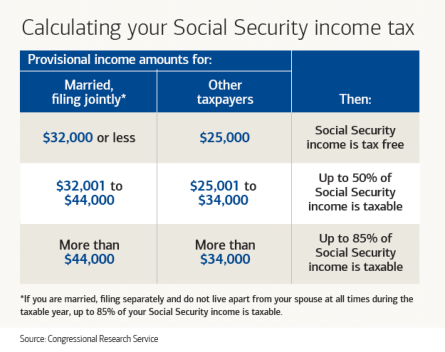

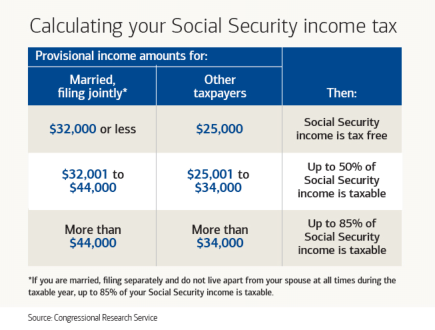

Many retirees begin taking Social Security benefits at Full Retirement Age in conjunction with beginning Medicare. Still, there is also an option to delay your Social Security benefits up to age 70 to receive a more significant benefit amount. However, did you know that Social Security benefits are up to 85% taxable? Because of this, additional income, or the combined income of over $44,000 for married filing jointly, could increase the taxability of your Social Security benefits from 50% to 85%, further increasing total income and, therefore, total taxes due.Is Social Security Taxable?

It depends -- Social Security benefits' taxability is based on a formula to calculate your combined income. It considers your Adjusted Gross Income (AGI) and one-half of your Social Security benefits. Taxability ranges from 0% to 85%. The good news is that 15% of Social Security benefits are always tax-free. Still, a lack of income planning when making withdrawals or implementing tax-savings strategies could push you from 0% to 85% taxability, inadvertently adding to your tax bill and creating tax inefficiencies quickly. Notice that while MAGI determines your Medicare brackets, your Adjusted Gross Income determines your Social Security tax. If your brain is spinning thinking of all of these variables of tax planning, you aren't alone. Tax planning isn't easy, but it's necessary, and it will help minimize your taxes in retirement and add value to your portfolio so that you can do more of the things you enjoy when you retire. Effective tax planning can also help you leave more to your beneficiaries.Proper Tax Planning: Leveraging Roth Conversions for Medicare Premiums & Social

Security Taxes

Tax Planning Strategy #1: Defer Taking Social Security One option is to consider whether it makes sense to defer taking Social Security until age 70. Deferring would not only allow them to take advantage of doing more significant Roth conversions for a few more years, but it would also allow them to increase their Social Security benefits while they wait. Tax Planning Strategy #2: Modify Roth Conversion Amount to Minimize Social Security Taxability Another option, if they want to begin to take Social Security at Full Retirement Age, is to modify the amount of Roth conversions they do each year. For example, instead of maxing out the 12% bracket, they could convert $44,000 instead of $80,000. Minimizing the conversion amount and overall income would keep the tax on their Social Security benefits to 50% rather than 85%. Tax Planning Strategy #3: Utilize Cash Flow Projections to Make Tax-Efficient Choices What if one used their IRA for spending and paying expenses while taking advantage of these tax strategies? Planning out spending during retirement is also crucial because withdrawals from pre-tax accounts are subject to ordinary income. Too much accumulation of taxable income from withdrawals could increase their Social Security taxability and increase their Medicare premium. There are many moving parts in effective tax planning, so understanding where you'll make withdrawals in retirement is of the utmost importance. The Medicare Premium and Social Security tax brackets don't determine every decision you'll make in retirement. However, our examples show what can happen if you aren't mindful of them while making financial and tax decisions. There will be instances where recognizing additional income or implementing tax strategies might be valuable enough to warrant an increase in your Medicare bracket or Social Security taxability. As they become relevant, you need to carefully consider your Medicare and Social Security tax brackets during ongoing tax planning. Often, we see these brackets overlooked by individuals and even their advisors or accountants. At Wink Inc, we do tax planning with our clients continuously to ensure that we see and optimize each piece of their tax situation. We help our clients plan efficient retirement withdrawals and decide the best times to recognize income. We also implement tax strategies after looking at a comprehensive view of their tax situation in a given year, considering all tax brackets before deciding on the best tax-saving strategies to take advantage of every year. We firmly believe taxes are an integral part of a comprehensive financial plan. Therefore, we hold that you and your advisor should always review taxes in coordination with your overall financial plan. While tax planning seems like a complicated and time-intensive process, it can make a substantial difference in taxes and savings over time when done correctly. Working with a financial advisor is beneficial to determine if this or other tax-efficient savings strategies can help you reach your long-term goals. Start the conversation with an advisor today. Choose the correct strategy’s to maximize your retirement assets and income. Make the correct choice on when and how to claim Social Security, a decsion that can affect your financial well being and family legacy. Please call us at (248) 816-1220 or 800-276-8319 to set up a free consultation. Or Book Your Consultation here: We service clients worldwide. Information presented is for educational purposes only. It should not be considered specific advice, does not take into consideration your specific situation, and does not intend to make an offer or solicitation for the adoption of any specific strategies. Be sure to consult with a qualified advisor and/or tax professional before implementing any strategy discussed herein. Be sure to have your specific situation reviewed prior to implimenting any strategies. Winc. Inc is a licensed Enrolled Agent firm.

Wink Inc. | Enrolled Agents | 2701 Troy Center Dr, Ste 430 | Troy | Michigan | 48084

Tel: 248-816-1220 | 800-276-8319 | Text: 248-800-6013|

Book Consultation

Book Consultation

Book Consultation

Book Consultation

Book Consultation

Book Consultation

Wink Inc.

Enrolled Agents

America’s Tax Experts

®

Wink Tax Services

Tax Planning for

Retirees: Social

Security and

Medicare Tax Rates.

Control Your Destiny

Medicare Tax Brackets Most begin Medicare at age 65, but did you know that your Medicare premium is based on your Modified Adjusted Gross Income from two years prior? That means that Medicare brackets matter as early as age 63. As we look at Medicare premium brackets and income each year, there's an additional complexity to be aware of. Medicare premium brackets are based on Modified Adjusted Gross Income (MAGI), which means they are unaffected by the standard or itemized deductions. As a result, income planning becomes more critical in Medicare brackets because you cannot offset your MAGI with mortgage interest, property tax, or charitable deductions.Income Planning for Medicare Premium

Brackets

So, we know this is an important consideration, but let's quantify just how important by looking at the Medicare premium brackets. The lowest monthly premium for Medicare is $170.10 per month per person, but the highest Medicare bracket is $578.30 per month. So, that's a $9,796.80 annual cost variance between the bottom and top bracket for those married filing jointly. Unlike income tax brackets where only the marginal dollars are taxed at the next tax bracket, when considering Medicare brackets, even just one additional dollar of MAGI will push your premiums to the next bracket for an entire year. IRMAA [Income Related Monthly Adjustment Amount] 2023What Is IRMAA? [Income Related Monthly Adjustment

Amount]

Medicare imposes surcharges on higher-income beneficiaries. The theory is that higher-income beneficiaries can afford to pay more for their healthcare. Instead of doing a 25:75 split with the government, they must pay a higher share of the program costs. The surcharge is called IRMAA, which stands for Income-Related Monthly Adjustment Amount. According to the Medicare Trustees Report, 8% of Medicare Part B and Part D beneficiaries paid IRMAA. The extra premiums they paid lowered the government’s share of the total Part B and Part D expenses by two percentage points. Big deal? The income used to determine IRMAA is your AGI plus muni bond interest from two years ago. Your current year income determines your IRMAA in 2 years. Your 2021 income determines your IRMAA in 2023. Your 2022 income determines your IRMAA in 2024. The untaxed Social Security benefits aren’t included in the income for determining IRMAA. As if it’s not complicated enough for not moving the needle much, IRMAA is divided into five income brackets. Depending on the income, higher-income beneficiaries pay 35%, 50%, 65%, 80%, or 85% of the program costs instead of 25%. The lines drawn for each bracket can cause a sudden jump in the premiums you pay. If your income crosses over to the next bracket by $1, all of a sudden your Medicare premiums can jump by over $1,000/year. If you are married and both of you are on Medicare, $1 more in income can make the Medicare premiums jump by over $1,000/year for each of you. IRMAA Appeal If your income two years ago was higher because you were working at that time and now your income is significantly lower because you retired (“work reduction” or “work stoppage”), you can appeal the IRMAA assessment. The “life-changing events” that make you eligible for an appeal include: • Death of spouse • Marriage • Divorce or annulment • Work reduction • Work stoppage • Loss of income from income producing property • Loss or reduction of certain kinds of pension income You file an appeal by filling out the form SSA-44 to show that although your income was higher two years ago, you had a reduction in income now due to one of the life-changing events above. For more information on the appeal, see Medicare Part B Premium Appeals.Not Penalized For Life

If your income two years ago was higher and you don’t have a life- changing event that makes you qualify for an appeal, you will pay the higher Medicare premiums for one year. IRMAA is re-evaluated every year as your income changes. If your higher income two years ago was due to a one-time event, such as realizing capital gains or taking a large withdrawal from your IRA, when your income comes down in the following year, your IRMAA will also come down automatically. It’s not the end of the world to pay IRMAA for one year. Roth Conversions Impact on Medicare Premiums Let's look at an example: Steve and Sara are both 63 years old, and they both have retired after successful careers. They do annual tax planning and make withdrawals from their after-tax accounts to fund living expenses so that they can do Roth conversions annually. Last year, at age 62, the only brackets they had to worry about were the income tax and capital gains tax brackets. However, at age 63, we need to start looking at their Medicare bracket. After retiring, Steve and Sara each receive pension benefits of $80,000 annually which puts them in the 22% income tax bracket for 2022. In addition, they take the standard deduction of $25,100. They also have substantial savings in IRAs and expect to have significant required minimum distributions at age 72 without taking any action. Previously, they converted IRA savings to Roth to max out their 22% income bracket, converting about $43,250 per year, which will reduce the size of their RMDs at age 72 and beyond). If they fail to think about Medicare brackets and Steve and Sara convert the same amount this year ($43,250), they will increase their Medicare premiums at age 65 from $170.10 per person per month to $238.10 per person per month. The annualized difference is approximately $1,600, but the effective tax rate on the conversion of $43,250 is now 25.7% instead of 22%. While this is only a $1,600 increase annually, it can add up year-over-year to a relatively significant number.The Common Mistake of DIY Tax Planning

Many choose to be even more aggressive to take advantage of the tax arbitrage provided by Roth conversions. For example, let's say that Steve and Sara know that their tax bracket will be significantly higher in the future than it is currently (22%). Therefore, they have been maxing out the 22% bracket and the 24% bracket, paying increased taxes now for lower required minimum distributions and associated taxes in the future. By doing this in 2022, they blow through the first few Medicare premium brackets and find themselves paying $442.30 each per month, an almost $5,000 annual increase in premiums per year. The effective tax rate on this conversion of $194,949 is 26.05% (24% ordinary income plus the additional Medicare premium of 2.05% ($5,000/$194,949). In this example, if Steve and Sara converted just $25,000 less, they could find themselves in a lower premium bracket with a lower effective tax rate of 25.6%. By properly planning their Roth conversions with a professional, they could save on premiums and taxes while also reaping the advantages of Roth conversions. These premiums may not be excessive enough to outweigh the benefits reaped from Roth conversions. Still, it is worth discussing converting slightly less in a given year to put them in a lower Medicare premium bracket. As noted, if you don't do this type of planning annually, the total premium increase year after year can add up! Remember, one dollar of MAGI can make the difference between a lower and higher Medicare bracket.Social Security Tax Brackets

Many retirees begin taking Social Security benefits at Full Retirement Age in conjunction with beginning Medicare. Still, there is also an option to delay your Social Security benefits up to age 70 to receive a more significant benefit amount. However, did you know that Social Security benefits are up to 85% taxable? Because of this, additional income, or the combined income of over $44,000 for married filing jointly, could increase the taxability of your Social Security benefits from 50% to 85%, further increasing total income and, therefore, total taxes due.Is Social Security Taxable?

It depends -- Social Security benefits' taxability is based on a formula to calculate your combined income. It considers your Adjusted Gross Income (AGI) and one-half of your Social Security benefits. Taxability ranges from 0% to 85%. The good news is that 15% of Social Security benefits are always tax-free. Still, a lack of income planning when making withdrawals or implementing tax-savings strategies could push you from 0% to 85% taxability, inadvertently adding to your tax bill and creating tax inefficiencies quickly. Notice that while MAGI determines your Medicare brackets, your Adjusted Gross Income determines your Social Security tax. If your brain is spinning thinking of all of these variables of tax planning, you aren't alone. Tax planning isn't easy, but it's necessary, and it will help minimize your taxes in retirement and add value to your portfolio so that you can do more of the things you enjoy when you retire. Effective tax planning can also help you leave more to your beneficiaries.Proper Tax Planning: Leveraging Roth

Conversions for Medicare Premiums & Social

Security Taxes

Tax Planning Strategy #1: Defer Taking Social Security One option is to consider whether it makes sense to defer taking Social Security until age 70. Deferring would not only allow them to take advantage of doing more significant Roth conversions for a few more years, but it would also allow them to increase their Social Security benefits while they wait. Tax Planning Strategy #2: Modify Roth Conversion Amount to Minimize Social Security Taxability Another option, if they want to begin to take Social Security at Full Retirement Age, is to modify the amount of Roth conversions they do each year. For example, instead of maxing out the 12% bracket, they could convert $44,000 instead of $80,000. Minimizing the conversion amount and overall income would keep the tax on their Social Security benefits to 50% rather than 85%. Tax Planning Strategy #3: Utilize Cash Flow Projections to Make Tax-Efficient Choices What if one used their IRA for spending and paying expenses while taking advantage of these tax strategies? Planning out spending during retirement is also crucial because withdrawals from pre-tax accounts are subject to ordinary income. Too much accumulation of taxable income from withdrawals could increase their Social Security taxability and increase their Medicare premium. There are many moving parts in effective tax planning, so understanding where you'll make withdrawals in retirement is of the utmost importance. The Medicare Premium and Social Security tax brackets don't determine every decision you'll make in retirement. However, our examples show what can happen if you aren't mindful of them while making financial and tax decisions. There will be instances where recognizing additional income or implementing tax strategies might be valuable enough to warrant an increase in your Medicare bracket or Social Security taxability. As they become relevant, you need to carefully consider your Medicare and Social Security tax brackets during ongoing tax planning. Often, we see these brackets overlooked by individuals and even their advisors or accountants. At Wink Inc, we do tax planning with our clients continuously to ensure that we see and optimize each piece of their tax situation. We help our clients plan efficient retirement withdrawals and decide the best times to recognize income. We also implement tax strategies after looking at a comprehensive view of their tax situation in a given year, considering all tax brackets before deciding on the best tax-saving strategies to take advantage of every year. We firmly believe taxes are an integral part of a comprehensive financial plan. Therefore, we hold that you and your advisor should always review taxes in coordination with your overall financial plan. While tax planning seems like a complicated and time-intensive process, it can make a substantial difference in taxes and savings over time when done correctly. Working with a financial advisor is beneficial to determine if this or other tax-efficient savings strategies can help you reach your long-term goals. Start the conversation with an advisor today. Choose the correct strategy’s to maximize your retirement assets and income. Make the correct choice on when and how to claim Social Security, a decsion that can affect your financial well being and family legacy. Please call us at (248) 816-1220 or 800-276-8319 to set up a free consultation. Or Book Your Consultation here: We service clients worldwide. Information presented is for educational purposes only. It should not be considered specific advice, does not take into consideration your specific situation, and does not intend to make an offer or solicitation for the adoption of any specific strategies. Be sure to consult with a qualified advisor and/or tax professional before implementing any strategy discussed herein. Be sure to have your specific situation reviewed prior to implimenting any strategies. Winc. Inc is a licensed Enrolled Agent firm.

Book Consultation

Book Consultation

Book Consultation

Book Consultation

Book Consultation

Book Consultation

Wink Inc. Enrolled Agents

2701 Troy Center Dr, Ste 430 | Troy | Michigan | 48084

Tel: 248-816-1220 | TF: 800-276-8319 | Text: 248-800-6013 |

- Home

- About

- Blog

- Disclosures

- Services

- Tax Preparation

- Tax Planning

- Accounting and Bookkeeping

- Business Consulting

- Business Formation

- Business Records Maintance Service

- Business Valuation

- Corporate Transparency Act CTA

- Divorce Services

- Drop-Off Service

- Future IRS Problems

- ITIN Certified Acceptance Agent (CAA) Service

- Notary Services

- Payroll Services

- Social Security Planning

- Medicare Tax Planning

- Unfiled Past Year Tax Returns

- Virtual Tax Service

- IRS Tax Problems Services

- Enrolled Agent (EA)

- Faq

- Library

- Resources

- Contact